2012 Annual Report

Information

Additional corporate information is available on our website: www.CTIpatents.com.

Additional copies of CopyTele’s Annual Report will are available to shareholders upon written request of Ron Tenio, Corporate Secretary, or by visiting http://ir.copytele.com.

Forward-Looking Statements: Statements that are not historical fact may be considered forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. Forward-looking statements are not statements of historical facts, but rather reflect CopyTele’s current expectations concerning future events and results. We generally use the words “believes,” “expects,” “intends,” “plans,” “anticipates,” “likely,” “will” and similar expressions to identify forward-looking statements. Such forward-looking statements, including those concerning our expectations, involve risks, uncertainties and other factors, some of which are beyond our control, which may cause our actual results, performance or achievements, or industry results, to be materially different from any future results, performance, or achievements expressed or implied by such forward-looking statements. These risks, uncertainties and factors include, but are not limited to, those factors set forth in “Item 1A – Risk Factors” and other sections of our Annual Report on Form 10-K for the fiscal year ended October 31, 2012 as well as in our Quarterly Reports on Form 10-Q and Current Reports on Form 8-K. We undertake no obligation to publicly update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except as required by law. You are cautioned not to unduly rely on such forward-looking statements when evaluating the information presented in this document.

Letter to Shareholder’s

Dear CTI Shareholders:

It is with great pleasure that I write my second letter to the shareholders of CTI. We have made great strides over the past year in stabilizing the company and in implementing our new business strategy. In this letter, I will briefly review the progress that we have made over the past year, discuss the items outlined in our Proxy Statement, and invite you all to attend our upcoming annual meeting on Friday, October 11, 2013 in New York.

As you are all aware, we brought in a new senior management team in September of 2012, to implement a new business model that includes the monetization of the patented technologies that we developed internally over the past several years. Robert Berman, our new President and CEO, and his team of former employees from Acacia Research Corporation, are experienced in, and have had a lot of success with, patent monetization and patent assertion.

Our new management team wasted no time in taking steps to unlock the hidden value in CTI’s patented technologies. In January of 2013, CTI sent AU Optronics Corp. a notice of termination of our License Agreement, and filed a lawsuit in the Federal District Court for the Northern District of California against AUO and E Ink Holdings, alleging breach of contract, fraud, conspiracy to monopolize, unfair business practices, antitrust, and other anti-competitive acts, and seeking punitive and treble damages, all in connection with the attempted misappropriation of CTI’s ePaper® Electrophoretic Display and Nano Field Emission Display technologies. CTI also brought a separate patent infringement lawsuit against E Ink. In June of 2013, CTI and AUO agreed to arbitrate CTI’s charges, which should result in a faster and more efficient adjudication. The Court also ordered E Ink to participate in the arbitration, for purposes of discovery. Because issues in the AUO/E Ink arbitration need to be resolved before the patent infringement case can proceed against E Ink, the Court dismissed the patent infringement case, without prejudice, meaning that CTI can re-file the patent infringement lawsuit, if necessary, following the arbitration.

In May of 2013, we launched our second patent assertion campaign by filing a patent infringement lawsuit in the Federal District Court for the Eastern District of New York against Microsoft Corporation in connection with the SKYPE video conferencing service and our patented Key Based Encryption web conferencing technology. In July of 2013, we followed up with similar lawsuits against Citrix Systems and Logitech International.

In addition to continuing to mine our own patents, we acquired the rights to two additional patent portfolios during the past year, including patent portfolios covering Loyalty Conversion Systems, and J-Channel Window Frame Construction. On August 7, 2013, we filed 8 separate patent infringement lawsuits in the Federal District Court for the Eastern District of Tennessee, against Lowe’s Companies, Clayton Homes, Pella Corporation, Jeld-Wen, Atrium Windows and Doors, Ply Gem Industries, RGF Industries, Tafco Corporation, Kinro Manufacturing, and Elixir Industries, all in connection with our patented J-Channel Window Frame technology. On August 20, 2013, we filed 10 separate patent infringement lawsuits in the Federal District Court for the Eastern District of Texas, against Alaska Airlines, American Airlines, Delta Airlines, Frontier Airlines, Hawaiian Airlines, JetBlue Airways, Southwest Airlines, Spirit Airlines, United Airlines, and U.S. Airways, all in connection with our Loyalty Conversion Systems patent portfolio.

In summary, we currently have 20 active lawsuits across 5 patented technologies. When considering our continuing efforts to mine our existing patents, the additional patent rights that we have already acquired, and several patent portfolios for which we are engaged in due diligence, we expect to be even more active in our patent monetization and patent assertion efforts in the coming year.

In order to help finance our ongoing operations and strengthen our financial condition, we closed two financings over the past 12 months. In January of 2013 we raised approximately $1.7 million in a private placement of convertible debentures that are convertible into shares of our common stock at a conversion price of $0.15 per share on or before January 25, 2015, and CTI may prepay the debentures at any time without penalty if certain conditions are met. In addition, on April 24, 2013, we entered into a common stock purchase agreement with the Aspire Capital Fund, LLC, whereby we have the right to require that Aspire Capital purchase up to $10 million of CopyTele’s common stock over a two year period, based upon prevailing market prices over a period preceding each sale. As part of this transaction, Aspire Capital made an initial purchase of $500,000 of CopyTele’s common stock at a price of $0.20 per share.

As pleased as I am with the progress that we have made with our patent assertion and patent monetization efforts, and with the financing transactions mentioned above, I am equally as pleased with the progress that we have made in the areas of investor relations and public relations. We have completely rebranded our company, and launched a modern, fully functional website that includes interesting and relevant videos, interviews, articles, and other information to better meet the needs of inventors, potential investors, and our existing shareholders. In addition to these cosmetic changes, we have embraced our commitment to making our existing shareholders a priority. All shareholder inquiries now receive a prompt response, and we have spent countless hours answering questions and explaining the intricacies of our new business strategy.

In addition to taking care of our existing shareholders, we have been a very active participant on the national stage in publishing content, making television appearances, and granting interviews in connection with our business activities and current issues that are relevant to us. Fox Business, CNN Money, The San Francisco Chronicle, Ad Week, Forbes, Seeking Alpha, TechCrunch, and Bloomberg are just a sample of the national media that have reported on our activities and sought our expertise. In addition to confirming our capabilities in the areas of patent assertion and patent monetization, these platforms have been very helpful in attracting inventors and new shareholders to our company.

Although we have accomplished much over the last 12 months, our transformation is still in its infancy. Last year, in our Proxy Statement, we requested a modest increase in the amount of our authorized shares, as a temporary measure to meet our immediate business needs. This year, with our transformation in full progress, we have asked for a more significant increase in the amount of our authorized shares, so that we have the capability to meet our future needs. As a public company in the patent monetization and patent assertion space, we need to have capacity to quickly and opportunistically grow our company, whether via acquisitions of individual patent portfolios, multiple portfolios, or entire companies. For these reasons, I ask that you approve the items set forth in the Proxy Statement in connection with our upcoming annual meeting, including the amendment to our charter to increase the amount of our authorized shares. Your positive response is needed in order for us to continue with our transformation. We need more than 50% of all stockholders to vote in the affirmative on this proposal, which we view as critical to being able to grow the company at an even faster pace. Failure to receive 50% of the vote will severely curtail our ability to execute our strategy and maximize stockholder value. For the future of the company, please vote yes.

This year, we will again be providing Internet access to our Proxy materials. In a separate mailing, you will receive a notice with instructions on how to obtain Proxy materials online or request a printed set.

Finally, I would like to invite each of you to attend our upcoming annual meeting scheduled for Friday, October 11, 2013, at the Fox Hollow in Woodbury, NY, at which time you will have the opportunity to meet with our Board members and management team.

Thank you and I look forward to seeing you there.

Sincerely,

Lewis H. Titterton, Jr.

Chairman

August 27, 2013

| UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C. 20549 | ||

| FORM 10-K | ||

|

| ||

| [x] ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended October 31, 2012 | ||

| or | ||

| [ ] TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the transition period from ___________ to ___________ | ||

| Commission file number: 0-11254 | ||

| COPYTELE, INC. | ||

| (Exact Name of Registrant as Specified in its Charter) | ||

| Delaware |

| 11-2622630 |

| (State or Other Jurisdiction of Incorporation or Organization) |

| (I.R.S. Employer Identification No.) |

| 900 Walt Whitman Road Melville, NY 11747 (631) 549-5900 | ||

| (Address, Including Zip Code, and Telephone Number, Including Area Code, of Registrant’s Principal Executive Offices)

| ||

| Securities registered pursuant to Section 12(b) of the Act: None | ||

| Securities registered pursuant to Section 12(g) of the Act: Common Stock, $.01 par value | ||

|

| ||

| Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes [_] No [x] | ||

| Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes [_] No [x] | ||

| Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes [x] No [_] | ||

| Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes [x] No [_] | ||

| Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. [ ] | ||

| Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. Large accelerated filer [__] Accelerated filer [__] Non-accelerated filer [__] (Do not check if a smaller reporting company) Smaller reporting company [x] | ||

| Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes [_] No [x] | ||

| Aggregate market value of the voting stock (which consists solely of shares of common stock) held by non-affiliates of the registrant as of April 30, 2012 (the last business day of the registrant’s most recently completed second fiscal quarter), computed by reference to the closing sale price of the registrant’s common stock on the Over-the-Counter Bulletin Board on such date ($0.165 ): $25,224,809 | ||

| On January 22, 2013, the registrant had outstanding 185,104,037 shares of common stock, par value $.01 per share, which is the registrant’s only class of common stock. | ||

|

DOCUMENTS INCORPORATED BY REFERENCE: NONE | ||

|

TABLE OF CONTENTS | ||

|

|

| Page |

| PART I |

| |

|

|

|

|

| Item 1. | Business | 2 |

| Item 1A. | Risk Factors | 8 |

| Item 1B. | Unresolved Staff Comments | 19 |

| Item 2. | Properties | 19 |

| Item 3. | Legal Proceedings | 19 |

|

|

| |

| PART II |

| |

|

|

|

|

| Item 5. | Market for Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities | 20 |

| Item 6. | Selected Financial Data | 24 |

| Item 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operations | 25 |

| Item 7A. | Quantitative and Qualitative Disclosures about Market Risk | 38 |

| Item 8. | Financial Statements and Supplementary Data | 39 |

| Item 9. | Changes in and Disagreements With Accountants on Accounting and Financial Disclosure | 39 |

| Item 9A. | Controls and Procedures | 40 |

| Item 9B. | Other Information | 40 |

|

|

| |

|

|

| |

| PART III |

| |

| Item 10. | Directors, Executive Officers and Corporate Governance | 40 |

| Item 11. | Executive Compensation | 44 |

| Item 12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | 58 |

| Item 13. | Certain Relationships and Related Transactions, and Director Independence | 62 |

| Item 14. | Principal Accounting Fees and Services | 64 |

|

|

| |

| PART IV |

| |

| Item 15. | Exhibits, Financial Statement Schedules | 64 |

1

PART I

Item 1. Business.

Forward-Looking Statements

Information included in this Annual Report on Form 10-K may contain forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. Forward-looking statements are not statements of historical facts, but rather reflect our current expectations concerning future events and results. We generally use the words “believes,” “expects,” “intends,” “plans,” “anticipates,” “likely,” “will” and similar expressions to identify forward-looking statements. Such forward-looking statements, including those concerning our expectations, involve risks, uncertainties and other factors, some of which are beyond our control, which may cause our actual results, performance or achievements, or industry results, to be materially different from any future results, performance or achievements expressed or implied by such forward-looking statements. These risks, uncertainties and factors include, but are not limited to, those factors set forth in this Annual Report on Form 10-K under “Item 1A. – Risk Factors” below. Except as required by applicable law, including the securities laws of the United States, we undertake no obligation to publicly update or revise any forward-looking statements, whether as a result of new information, future events or otherwise. You are cautioned not to unduly rely on such forward-looking statements when evaluating the information presented in this Annual Report on Form 10-K.

Overview

As used herein, “we,” “us,” “our,” the “Company”, “CopyTele” or “CTI” means CopyTele, Inc. unless otherwise indicated. Unless otherwise indicated, all references in this Form 10-K to “dollars” or “$” refer to US dollars.

CTI currently owns 53 U.S. patents and 11 U.S. patent applications. Our principal operations include the development, acquisition, licensing, and enforcement of patented technologies. While in the past, the primary operations of the Company involved licensing in connection with and the development of patented technologies, the primary operations of the Company going forward will be patent licensing in connection with the unauthorized use of patented technologies and patent enforcement. We expect to first generate revenues and related cash flows from the licensing and enforcement of patents that we currently own. We are continuing to develop our patent portfolios through the filing and prosecution of patent applications and will initiate lawsuits, if necessary, to prevent the unauthorized use of our patented technologies. Certain of our patents are encumbered due to arrangements previously entered into by the Company. Where we are able, we will take the steps necessary to remove any encumbrances that may inhibit our patent licensing and enforcement efforts. We expect to obtain the rights to license and enforce additional patents from third parties, and when necessary, will assist such parties in the further development of their patent portfolios through the filing of additional patent applications. In the ordinary course of our business, we will likely initiate patent enforcement actions against unauthorized users of patented technologies on our own behalf and in conjunction with such third parties.

2

Patent Monetization and Patent Assertion

Patent monetization is the generation of revenue and proceeds from patents and patented technologies (“Patent Monetization”). Patent assertion is a specialized type of Patent Monetization where a patent owner, or a representative of the patent owner, seeks to prohibit or collect royalties from the unauthorized manufacture, sale, and use of the owner’s patented invention (“Patent Assertion”). CTI’s new business model is Patent Monetization and Patent Assertion. We currently own 53 U.S. patents and 11 U.S. patent applications, which are mainly grouped into 4 patent portfolios: Key Based Encryption (“KB Encryption”); ePaper® Electrophoretic Display (“ePaper® Display”); Nano Field Emission Display (“nFED Display”); and Micro Electro Mechanical Systems Display (“MEMS Display”).

CTI’s Patent Portfolios

Key Based Encryption

Portfolio covering the generation and management of encryption keys used for securing e-mail, text messages, data, voice and facsimile. This type of encryption technology is commonly used for cloud based storage and email archiving, to comply with HIPAA and other regulations regarding the safeguarding of personal information. KB Encryption can also be used for protecting sensitive cellular, satellite, and local area network communications.

ePaper® Electrophoretic Display

Fundamental portfolio covering the underlying chemistry, manufacturing, assembly, and internal operations of core electrophoretic technology used in the world’s most popular eReader devices. Coverage includes both the particles, and the suspension, which are the primary elements used to create highly reflective grey scale images to simulate reading on paper.

Nano Field Emission Display

Portfolio covering a new type of flat panel display consisting of low voltage color phosphors, specially coated carbon nanotubes, nano materials to generate secondary electrons, and ionized noble gas, resulting in a bright, sharp, high contrast color image. This is an emerging technology that would result in a flat panel display utilizing less power, with better picture quality and lower manufacturing costs.

Micro Electro Mechanical Systems Display

Portfolio covering vanadium dioxide coated pixels that electrically modulate light at extremely high speeds to form an image. Additional coverage on use of electrostatic force to move pixel sized membranes that create a color image. These are emerging, low voltage, display technologies with numerous potential commercial applications.

3

Under the terms of the Videocon License Agreement, we were scheduled to receive a license fee of $11 million from Videocon, payable in installments over a 27 month period and an agreed upon royalty from Videocon based on display sales by Videocon. The initial installment was received in May 2008 however certain license fee payments were subsequently deferred. The deferral of the license fee payments is no longer in effect; however, we cannot give any assurance that additional license fees will be received. No license fee payments were received from Videocon during the fiscal years ended October 31, 2012 and 2011. As of October 31, 2012, we have received aggregate license fee payments from Videocon of $3.2 million and $7.8 million remains owed to us.

At the same time we entered into the Videocon License Agreement in November 2007, we also entered into a Share Subscription Agreement (the “Share Subscription Agreement”) with Mars Overseas Limited, an affiliate of Videocon (“Mars Overseas”). Under the Share Subscription Agreement, Mars Overseas purchased 20,000,000 unregistered shares of our common stock (the “CopyTele Shares”) from us for an aggregate purchase price of $16,200,000. Also in November 2007, our wholly-owned subsidiary, CopyTele International Ltd. (“CopyTele International”), entered into a GDR Purchase Agreement with Global EPC Ventures Limited (“Global”), for CopyTele International to purchase from Global 1,495,845 global depository receipts of Videocon (the “Videocon GDRs”) for an aggregate purchase price of $16,200,000.

For the purpose of effecting a lock up of the Videocon GDRs and CopyTele Shares (collectively, the “Securities”) for a period of seven years, and therefore restricting both parties from selling or transferring the Securities during such period, CopyTele International and Mars Overseas entered into two Loan and Pledge Agreements in November 2007. The Videocon GDRs are to be held as security for a loan in the principal amount of $5,000,000 from Mars Overseas to CopyTele International, and the CopyTele Shares are similarly held as security for a loan in the principal amount of $5,000,000 from CopyTele International to Mars Overseas. The loans are for a period of seven years, do not bear interest, and prepayment of the loans will not release the lien on the Securities prior to end of the seven year period. The loan agreements provide for customary events of default, which may result in forfeiture of the Securities by the defaulting party, and also provide for the transfer to the respective parties, free and clear of any encumbrances under the agreements, any dividends, distributions, rights or other proceeds or benefits in respect of the Securities. The loan receivable from Mars Overseas is classified as a contra-equity under shareholders’ equity in the accompanying consolidated balance sheet, because the loan receivable is secured by the CopyTele Shares and the Share Subscription Agreement and Loan and Pledge Agreement were entered into concurrently. We have entered into discussions with Videocon regarding the disposition of the Subscriptions Agreements, and Loan and Pledge Agreements.

Volga Svet Ltd.

In September 2009, we entered into a Technology License Agreement with Volga Svet Ltd., (the “Volga License Agreement”) to produce and market our thin, flat, low voltage phosphor, Nano Displays in Russia. In addition, in September 2009, we entered into a separate agreement with Volga whereby we obtained a 19.9% ownership interest in Volga in exchange for 150,000 unregistered shares of our common stock. Since we do not anticipate that we will continue to develop our Nano Displays, we are re-evaluating the Volga License Agreement and our ownership interest in Volga.

5

ZQX Advisors LLC

In August of 2009, we initiated an evaluation of our ePaper® Electrophoretic Display technology under an agreement with ZQX Advisors LLC (“ZQX”) and took a 19.5% ownership interest in ZQX. On January 21, 2013 we terminated our agreement with ZQX, but currently retain our 19.5% interest in ZQX.

Encryption Products

We continue to look for opportunities to sell off our remaining inventory of encryption products and have arrangements to support those products as necessary in connection with any such sales. We do not anticipate developing any additional encryption products.

Competition

CTI expects to encounter competition in the areas of patent acquisitions and enforcement from both private and publicly traded companies that engage in Patent Monetization and Patent Assertion. This includes competition from companies seeking to acquire the same patents and patent rights that we may seek to acquire. Entities such as Acacia Research Corporation, Allied Security Trust, Altitude Capital Partners, Coller IP, Intellectual Ventures, Millennium Partners, Open Innovation Network, RPX Corporation, Rembrandt IP Management, and others derive all or a substantial portion of their revenue from Patent Assertion and we expect more entities to enter the market.

We also compete with venture capital firms, strategic corporate buyers and various industry leaders for patent and technology acquisitions and licensing opportunities. Many of these competitors have more financial and human resources than our company.

Research and Development

Research and development expenses were approximately $2866,000 and $2,873,000 for the fiscal years ended October 31, 2012 and 2011, respectively. In accordance with the changes in the primary operations of the Company during the fourth quarter of fiscal year 2012, we are no longer incurring research and development expenses. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations” below and our Consolidated Financial Statements.

Employees

As of December 31, 2012, we had 7 full-time employees.

6

Regulation

Our international sales of our encryption devices, technology and software solutions are subject to U.S. and foreign regulations such as the International Traffic in Arms Regulations (“ITAR”) and Export Administration Regulations and may require licenses (including export licenses) from U.S. government agencies or require the payment of certain tariffs. In addition, in accordance with applicable regulations, we file the requisite semiannual reports on exports of these products with the applicable U.S. government agencies. Our ability to export in the future is dependent upon our ability to obtain the export authorizations from the appropriate U.S. government agency. In addition, in accordance with Export Administration Regulations, without a valid export license, we are prohibited from exporting these products to any country that the U.S. State Department has identified as state sponsors of terrorism and are subject to U.S. economic sanctions and export controls, which include Cuba, Iran, Sudan and Syria. However, neither we nor any of our subsidiaries have ever exported, or currently anticipate exporting, any goods or services to any such countries either directly or to our knowledge, indirectly through any distributor or licensee, nor have we ever had, or anticipate in the future having, any direct or indirect arrangements or other contacts with the governments of those countries or entities controlled by those governments. Furthermore, before we make any domestic or international shipments of encryption equipment, software or technology, we confirm that the recipient is not on any denied person or similar list maintained by the U.S. Department of Commerce, Bureau of Industry and Security.

Other

On November 30, 2012, our stockholders’ approved an amendment to our certificate of incorporation to increase the number of shares of common stock we are authorized to issue from 240 million to 300 million.

We were incorporated on November 5, 1982 under the laws of the State of Delaware. Our principal executive offices are located at 900 Walt Whitman Road, Melville, New York 11747, our telephone number is 631-549-5900, and our Internet website address is www.copytele.com. We make available free of charge on or through our Internet website our annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, proxy statements on Schedule 14A, and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934, as amended (the “Exchange Act”) as soon as reasonably practicable after we electronically file such materials with, or furnish them to, the Securities and Exchange Commission (the “Commission”). Alternatively, you may also access our reports at the SEC’s website at www.sec.gov. You may also read and copy any document we file with the SEC at the SEC’s public reference room located at 100 F Street, NE, Washington, DC 20549, on official business days during the hours of 10:00 a.m. and 3:00 p.m. Please call the SEC at 1-800-SEC-0330 for further information on the operation of the public reference room.

Financial Information About Segments and Geographical Areas

See our Consolidated Financial Statements.

7

Item 1A. Risk Factors.

Our business involves a high degree of risk and uncertainty, including the following risks and uncertainties:

Risks Related to Our Financial Condition and Operations

We have a history of losses and may incur additional losses in the future.

On a cumulative basis we have sustained substantial losses and negative cash flows from operations since our inception. As of October 31, 2012, our accumulated deficit was approximately $125,083,000. As of October 31, 2012, we had approximately $840,000 in cash, cash equivalents and short-term investments on hand, and negative working capital of approximately $900,000. We expect to continue incurring significant legal and general and administrative expenses in connection with our operations. As a result, we anticipate that we may incur losses in the future.

We may need additional funding in the future which may not be available on acceptable terms and, if available, may result in dilution to our stockholders, and the report from our independent registered public accountants includes an uncertainty paragraph regarding our ability to continue as a going concern.

Based on currently available information, we believe that our existing cash, cash equivalents, and short-term investments, together with expected cash flows from patent licensing and enforcement, and other potential sources of cash flow may not be sufficient to enable us to continue our patent licensing and enforcement activities for at least 12 months. However, our projections of future cash needs and cash flows may differ from actual results. If current cash on hand and cash that may be generated from patent licensing and enforcement activities are insufficient to satisfy our liquidity requirements, we may seek to sell our investment securities or other financial assets or our debt or additional equity securities or obtain loans from various financial institutions where possible. The sale of additional equity securities or securities convertible into or exercisable for equity securities could result in dilution to our shareholders. We can give no assurance that we will generate sufficient cash flows in the future (through licensing and enforcement of patents, or otherwise) to satisfy our liquidity requirements or sustain future operations, or that other sources of funding, such as sales of equity or debt, would be available, if needed, on favorable terms or at all. If we cannot obtain such funding if needed or if we cannot sufficiently reduce operating expenses, we would need to curtail or cease some or all of our operations.

As shown in the accompanying consolidated financial statements, we have incurred a net loss of approximately $4,253,000 during the fiscal year ended October 31, 2012, and, as of that date, we have an accumulated deficit of approximately $125,083,000 and a net shareholders’ equity deficit of approximately $1,194,000. These and the other factors described herein raise uncertainty about our ability to continue as a going concern. Management’s plans in regard to these matters are set forth above. The accompanying financial statements have been prepared assuming that we will continue as a going concern and do not include any adjustments that might result from the outcome of this uncertainty. The report from our independent registered public accountants, KPMG LLP, dated January 29, 2013, includes an explanatory paragraph related to our ability to continue as a going concern.

8

If we encounter unforeseen difficulties with our business or operations in the future that require us to obtain additional working capital, and we cannot obtain additional working capital on favorable terms, or at all, our business may suffer.

Our consolidated cash, cash equivalents and short-term investments on hand totaled approximately $840,000 and $3,023,000 at October 31, 2012 and 2011, respectively. To date, we have relied primarily upon cash from our operations and from the public and private sale of equity securities to generate the working capital needed to finance our operations.

We may encounter unforeseen difficulties with our business or operations in the future that may deplete our capital resources more rapidly than anticipated. As a result, we may be required to obtain additional working capital in the future through bank credit facilities, public or private debt or equity financings, or otherwise. If we are required to raise additional working capital in the future, such financing may be unavailable to us on favorable terms, if at all, or may be dilutive to our existing stockholders. If we fail to obtain additional working capital as and when needed, such failure could have a material adverse impact on our business, results of operations and financial condition.

Failure to effectively manage our potential growth could place strains on our managerial, operational and financial resources and could adversely affect our business and operating results.

Our potential growth is expected to place a strain on our managerial, operational and financial resources and systems. Further, as our business grows, we will be required to manage multiple relationships. Any growth by us, or an increase in the number of our strategic relationships, may place additional strain on our managerial, operational and financial resources and systems. Although we may not grow as we expect, if we fail to manage our growth effectively or to develop and expand our managerial, operational and financial resources and systems, our business and financial results will be materially harmed.

Our future success depends on our ability to expand our organization.

As we grow, the administrative demands upon us will grow, and our success will depend upon our ability to meet those demands. These demands include increased accounting, management, legal services, staff support, and general office services. We may need to hire additional qualified personnel to meet these demands, the cost and quality of which is dependent in part upon market factors outside of our control. Further, we will need to effectively manage the training and growth of our staff to maintain an efficient and effective workforce, and our failure to do so could adversely affect our business and operating results.

9

Our investments are subject to risks, which may cause us to incur losses or have reduced liquidity.

The capital and credit markets have been experiencing extreme volatility and disruption since 2008, and at times, the volatility and disruption have reached unprecedented levels. In some cases, the markets have exerted downward pressure on stock prices and credit capacity for certain issuers. Although economic conditions appear to be improving, if the current capital and credit markets do not continue to improve or further deteriorate, we may be unable to liquidate a particular issue. Furthermore, if economic conditions do not continue to improve, or if they further deteriorate, we may be required to record additional impairment charges in a future period despite our ability to hold such investments until maturity.

Our equity arrangements with Videocon involve market risks.

At the same time as we entered into the Videocon License Agreement, we entered into the Share Subscription Agreement with Mars Overseas, to purchase the 20,000,000 CopyTele Shares, and our subsidiary, CopyTele International, entered into the GDR Purchase Agreement to purchase the 1,495,845 Videocon GDRs. The value of the Videocon GDRs owned by us depends upon, among other things, the value of Videocon’s securities in its home market of India, as well as exchange rates between the U.S. dollar and Indian rupee (the currency in which Videocon’s securities are traded in its home market). Based on both the duration and the continuing magnitude of the market price declines and the uncertainty of recovery, we recorded other than temporary impairments as of October 31, 2009 and 2011. We can give no assurances that the value of the Videocon GDRs will not decline in the future and future write downs may occur.

In addition, for the purpose of effecting a lock up of the Videocon GDRs and CopyTele Shares (collectively, the “Securities”) for a period of seven years, and therefore restricting both parties from selling or transferring the Securities during such period, CopyTele International and Mars Overseas entered into two Loan and Pledge Agreements. The Videocon GDRs are to be held as security for a loan in the principal amount of $5,000,000 from Mars Overseas to CopyTele International, and the CopyTele Shares are similarly held as security for a loan in the principal amount of $5,000,000 from CopyTele International to Mars Overseas. The loans are for a term of seven years, do not bear interest and prepayment of the loans will not release the lien on the Securities prior to the end of the seven year period. The loan agreements also provide for customary events of default which may result in forfeiture of the Securities by the defaulting party. We can give no assurances that the respective parties receiving such loans will not default on such loans.

Risks Related to Patent Monetization and Patent Assertion Activities

We may not be able to monetize our patent portfolios.

As we recently announced, the primary operations of the Company going forward will be Patent Monetization and Patent Assertion. We expect to first generate revenues and related cash flows from the licensing and enforcement of patents that we currently own and we expect to obtain the rights to license and enforce additional patents from third parties. However, we can give no assurances that we will be able to identify opportunities to exploit such patents or that such opportunities, even if identified, will generate sufficient revenues to sustain future operations.

10

Certain of our patent portfolios are subject to existing license agreements with AUO and Videocon which may limit our ability to monetize them.

In the course of entering into the EPD License Agreement and the Nano Display License Agreement with AUO, and the Videocon License Agreement with Videocon, certain rights to our ePaper® Display patents were licensed to AUO, and certain rights to our nFED Display patents were licensed to AUO and Videocon, respectively. We have terminated the EPD License Agreement and the Nano Display License Agreement with AUO although we can give no assurance that AUO will not challenge the effectiveness of such terminations, and we are engaged in discussions with Videocon with respect to the Videocon License Agreement. We intend to take the steps necessary to seek to remove any encumbrances that may inhibit our patent licensing and enforcement efforts; however, we can give no assurance that the ePaper® Display patents and the nFED patents will be unencumbered. If the patent portfolios remain encumbered or if our termination of the AUO license agreements are deemed to be ineffective, it could limit our ability to monetize such portfolios.

While we recently commenced lawsuits against AUO and E Ink, we may not be successful in obtaining judgments in our favor.

While we recently filed the AUO/E Ink Lawsuit and the E Ink Lawsuit, we can give no assurance that these lawsuits will be decided in our favor or even if they are that the damages and other remedies will be material.

Our revenues are unpredictable, and this may harm our financial condition.

Due to the nature of the licensing business and uncertainties regarding the amount and timing of the receipt of license and other fees from potential infringers, stemming primarily from uncertainties regarding the outcome of enforcement actions, rates of adoption of our patented technologies, the growth rates of potential licensees and certain other factors, our revenues may vary significantly from quarter to quarter, which could make our business difficult to manage, adversely affect our business and operating results, cause our quarterly results to fall below market expectations and adversely affect the market price of our common stock.

Our success depends in part upon our ability to retain the best legal counsel to represent us in patent enforcement litigation.

The success of our licensing business depends upon our ability to retain the best legal counsel to prosecute patent infringement litigation. As our patent enforcement actions increase, it will become more difficult to find the best legal counsel to handle all of our cases because many of the best law firms may have a conflict of interest that prevents their representation of us.

11

We, in certain circumstances, rely on representations, warranties and opinions made by third parties that, if determined to be false or inaccurate, may expose us to certain material liabilities.

From time to time, we may rely upon the opinions of purported experts. In certain instances, we may not have the opportunity to independently investigate and verify the facts upon which such opinions are made. By relying on these opinions, we may be exposed to liabilities in connection with the licensing and enforcement of certain patents and patent rights which could have a material adverse effect on our operating results and financial condition.

Once we commence Patent Monetization and Patent Assertion, we may become subject to claims and counterclaims by third parties.

As we become engaged in the business of Patent Monetization and Patent Assertion, we may be subject to claims, counterclaims and legal actions that arise in the ordinary course of business and which could have a material impact on our operation and financial condition. In connection with any of patent enforcement actions, it is also possible that a defendant may request and/or a court may rule that we have violated statutory authority, regulatory authority, federal rules, local court rules, or governing standards relating to the substantive or procedural aspects of such enforcement actions. In such event, a court may issue monetary sanctions against us or award attorney's fees and/or expenses to a defendant(s), which could be material.

Our exposure to uncontrollable outside influences, including new legislation, court rulings or actions by the United States Patent and Trademark Office, could adversely affect our Patent Monetization and Patent Assertion business and results of operations.

Our Patent Monetization and Patent Assertion business is subject to numerous risks from outside influences, including the following:

New legislation, regulations or rules related to obtaining patents or enforcing patents could significantly increase our operating costs and decrease our revenue.

We may apply for patents and may spend a significant amount of resources to enforce those patents. If new legislation, regulations or rules are implemented either by Congress, the U.S. Patent and Trademark Office (“USPTO”), or the courts that impact the patent application process, the patent enforcement process or the rights of patent holders, these changes could negatively affect our expenses and revenue. For example, new rules regarding the burden of proof in patent enforcement actions could significantly increase the cost of our enforcement actions, and new standards or limitations on liability for patent infringement could negatively impact our revenue derived from such enforcement actions.

Trial judges and juries often find it difficult to understand complex patent enforcement litigation, and as a result, we may need to appeal adverse decisions by lower courts in order to successfully enforce our patents.

It is difficult to predict the outcome of patent enforcement litigation at the trial level. It is often difficult for juries and trial judges to understand complex, patented technologies, and as a result, there is a higher rate of successful appeals in patent enforcement litigation than more standard business litigation. Such appeals are expensive and time consuming, resulting in increased costs and delayed revenue. Although we diligently pursue enforcement litigation, we cannot predict with significant reliability the decisions made by juries and trial courts.

More patent applications are filed each year resulting in longer delays in getting patents issued by the USPTO.

We hold a number of pending patents. We have identified a trend of increasing patent applications each year, which we believe is resulting in longer delays in obtaining approval of pending patent applications. The application delays could cause delays in recognizing revenue from these patents and could cause us to miss opportunities to license patents before other competing technologies are developed or introduced into the market.

U.S. Federal courts are becoming more crowded, and as a result, patent enforcement litigation is taking longer.

Patent enforcement actions are almost exclusively prosecuted in U.S. Federal court. Federal trial courts that hear patent enforcement actions also hear criminal cases. Criminal cases always take priority over patent enforcement actions. As a result, it is difficult to predict the length of time it will take to complete an enforcement action. Moreover, we believe there is a trend in increasing numbers of civil lawsuits and criminal proceedings before United States Judges, and as a result, we believe that the risk of delays in patent enforcement actions will have a significant effect on our business in the future unless this trend changes.

Any reductions in the funding of the USPTO could have an adverse impact on the cost of processing pending patent applications and the value of those pending patent applications.

Our primary asset is our patent portfolios, including pending patent applications before the USPTO. The value of our patent portfolios is dependent upon the issuance of patents in a timely manner, and any reductions in the funding of the USPTO could negatively impact the value of our assets. Further, reductions in funding from Congress could result in higher patent application filing and maintenance fees charged by the USPTO, causing an unexpected increase in our expenses.

Competition is intense in the industries in which we do business and as a result, we may not be able to grow or maintain our market share for our technologies and patents.

Our licensing business may compete with venture capital firms and various industry leaders for technology licensing opportunities. Many of these competitors may have more financial and human resources than we do. As we become more successful, we may find more companies entering the market for similar technology opportunities, which may reduce our market share in one or more technology industries that we currently rely upon to generate future revenue.

13

Our patented technologies face uncertain market value.

Many of our patents and technologies are in the early stages of adoption in the commercial and consumer markets. Demand for some of these technologies is untested and is subject to fluctuation based upon the rate at which our licensees will adopt our patents and technologies in their products and services.

As patent enforcement litigation becomes more prevalent, it may become more difficult for us to voluntarily license our patents.

We believe that the more prevalent patent enforcement actions become, the more difficult it will be for us to voluntarily license our patents. As a result, we may need to increase the number of our patent enforcement actions to cause infringing companies to license the patent or pay damages for lost royalties. This may increase the risks associated with an investment in our company.

Uncertainty in global economic conditions could negatively affect our business, results of operations and financial condition.

Our revenue-generating opportunities depend on the use of our patented technologies by existing and prospective licensees, the overall demand for the products and services of our licensees, and on the overall economic and financial health of our licensees. Although economic conditions appear to be improving, recent uncertainties in global economic conditions have resulted in a tightening of the credit markets, a low level of liquidity in many financial markets, and extreme volatility in the credit, equity and fixed income markets. If economic conditions do not continue to improve, or if they further deteriorate, many of our licensees' potential customers, which may rely on credit financing, may delay or reduce their purchases of our licensees' products and services. In addition, the use or adoption of our patented technologies is often based on current and forecasted demand for our licensees' products and services in the marketplace and may require companies to make significant initial commitments of capital and other resources. If negative conditions in the global credit markets delay or prevent our licensees' and their potential customers' access to credit, overall consumer spending on the products and services of our licensees may decrease and the potential adoption or use of our patented technologies may slow, respectively. Further, if the markets in which our licensees' intend to participate do not continue to improve, or deteriorate further, this could negatively impact our licensees' long-term sales and revenue generation, margins and operating expenses, which could in turn have an adverse effect on our future business, results of operations and financial condition.

In connection with patent enforcement actions conducted by us, a court may rule that we have violated certain statutory, regulatory, federal, local or governing rules or standards, which may expose us to certain material liabilities.

In connection with any of our patent enforcement actions, it is possible that a defendant may request and/or a court may rule that we have violated statutory authority, regulatory authority, federal rules, local court rules, or governing standards relating to the substantive or procedural aspects of such enforcement actions. In such event, a court may issue monetary sanctions against us or award attorney's fees and/or expenses to a defendant(s), which could be material, and if we are required to pay such monetary sanctions, attorneys' fees and/or expenses, such payment could materially harm our operating results and our financial position.

We are dependent upon a few key personnel and the loss of their services could adversely affect us.

Our future success to monetize our patent portfolios will depend on the efforts of our President and Chief Executive Officer, Robert A. Berman, and our Senior Vice President – Engineering, John Roop, and our strategic advisor, Dr. Amit Kumar. We do not maintain “key person” life insurance on Messrs. Berman or Roop or Dr. Kumar. The loss of the services of any such persons could have a material adverse effect on our business and operating results.

Risks Related to Our Common Stock

The availability of shares for sale in the future could reduce the market price of our common stock.

In the future, we may issue securities to raise cash for operations and acquisitions. We have and in the future may issue securities convertible into our common stock. Any of these events may dilute stockholders' ownership interests in our company and have an adverse impact on the price of our common stock.

In addition, sales of a substantial amount of our common stock in the public market, or the perception that these sales may occur, could reduce the market price of our common stock. This could also impair our ability to raise additional capital through the sale of our securities.

We have a limited number of common shares available for future issuance which could adversely affect our ability to raise capital.

We are authorized to issue 300,000,000 shares of common stock. As of January 25, 2013, we have outstanding 185,104,037 shares of common stock or 280,532,256 shares of common stock after giving effect to the assumed exercise of all outstanding warrants and options and assumed conversion of convertible debentures. Due to the limited number of authorized shares available for issuance, we may not able to raise significant additional capital until we increase the number of shares we are authorized to issue. To facilitate the possibility and flexibility of raising of additional capital or the completion of potential acquisitions of patent portfolios, we will seek stockholder approval to increase the number of our authorized shares of common stock. We can provide no assurance that stockholders will approve an amendment to our certificate of incorporation to increase the number of shares of common stock we are authorized to issue. If we require additional capital and we are unable to obtain stockholder approval of increase the number of shares of common stock, we would need to curtail or cease some or all of our operations.

15

Delaware law and our charter documents contain provisions that could discourage or prevent a potential takeover of our company that might otherwise result in our stockholders receiving a premium over the market price of their shares.

Provisions of Delaware law and our certificate of incorporation and bylaws could make the acquisition of our company by means of a tender offer, proxy contest or otherwise, and the removal of incumbent officers and directors, more difficult. These provisions include:

· Section 203 of the Delaware General Corporation Law, which prohibits a merger with a 15%-or-greater stockholder, such as a party that has completed a successful tender offer, until three years after that party became a 15%-or-greater stockholder;

· The authorization in our certificate of incorporation of undesignated preferred stock, which could be issued without stockholder approval in a manner designed to prevent or discourage a takeover; and

· Provisions in our bylaws regarding stockholders' rights to call a special meeting of stockholders limit such rights to stockholders holding together at least a majority of shares of the Company entitled to vote at the meeting, which could make it more difficult for stockholders to wage a proxy contest for control of our board of directors or to vote to repeal any of the anti-takeover provisions contained in our certificate of incorporation and bylaws.

Together, these provisions may make the removal of management more difficult and may discourage transactions that could otherwise involve payment of a premium over prevailing market prices for our common stock.

We may fail to meet market expectations because of fluctuations in quarterly operating results, which could cause the price of our common stock to decline.

Our reported revenues and operating results have fluctuated in the past and may continue to fluctuate significantly from quarter to quarter in the future. It is possible that in future periods, revenues could fall below the expectations of securities analysts or investors, which could cause the market price of our common stock to decline. The following are among the factors that could cause our operating results to fluctuate significantly from period to period:

· the dollar amount of agreements executed in each period, which is primarily driven by the nature and characteristics of the technology being licensed and/or the magnitude of infringement associated with a specific licensee;

· the specific terms and conditions of agreements executed in each period and/or the periods of infringement contemplated by the respective payments;

· fluctuations in the total number of agreements executed;

· fluctuations in the sales results or other royalty-per-unit activities of our licensees that impact the calculation of license fees due;

· the timing of the receipt of periodic license fee payments and/or reports from licensees;

· fluctuations in the net number of active licensees period to period;

· costs related to acquisitions, alliances, licenses and other efforts to expand our operations;

· the timing of payments under the terms of any customer or license agreements into which we may enter; and

· expenses related to, and the timing and results of, patent filings and other enforcement proceedings relating to intellectual property rights, as more fully described in this section.

16

Technology company stock prices are especially volatile, and this volatility may depress the price of our common stock.

The stock market has experienced significant price and volume fluctuations, and the market prices of technology companies have been highly volatile. We believe that various factors may cause the market price of our common stock to fluctuate, perhaps substantially, including, among others, the following:

· announcements of developments in our patent enforcement actions;

· developments or disputes concerning our patents;

· our or our competitors' technological innovations;

· developments in relationships with licensees;

· variations in our quarterly operating results;

· our failure to meet or exceed securities analysts' expectations of our financial results;

· a change in financial estimates or securities analysts' recommendations;

· changes in management's or securities analysts' estimates of our financial performance;

· changes in market valuations of similar companies;

· the current sovereign debt crises affecting several countries in the European Union and concerns about sovereign debt of the United States;

· announcements by us or our competitors of significant contracts, acquisitions, strategic partnerships, joint ventures, capital commitments, new technologies, or patents; and

· failure to complete significant transactions.

The financial crisis affecting the banking system and financial markets and the uncertainty in global economic conditions, which began in late 2007 has resulted in a tightening in the credit markets, a low level of liquidity in many financial markets, and extreme volatility in the credit, equity and fixed income markets. As noted above, our stock price, like many others, has fluctuated significantly in recent periods and if investors have concerns that our business, operating results and financial condition will be negatively impacted by global economic conditions, our stock price could continue to fluctuate significantly in future periods.

In addition, we believe that fluctuations in our stock price during applicable periods can also be impacted by court rulings and/or other developments in our patent licensing and enforcement actions. Court rulings in patent enforcement actions are often difficult to understand, even when favorable or neutral to the value of our patents and our overall business, and we believe that investors in the market may overreact, causing fluctuations in our stock prices that may not accurately reflect the impact of court rulings on our business operations and assets.

17

In the past, companies that have experienced volatility in the market price of their stock have been the objects of securities class action litigation. If our common stock was the object of securities class action litigation, it could result in substantial costs and a diversion of management's attention and resources, which could materially harm our business and financial results.

Our common stock is subject to the Commission’s penny stock rules which may make our shares more difficult to sell.

Our common stock fits the definition of a penny stock and therefore is subject to the rules adopted by the Commission regulating broker-dealer practices in connection with transactions in penny stocks. The Commission’s rules may have the effect of reducing trading activity in our common stock making it more difficult for investors to sell their shares. The Commission’s rules require a broker or dealer proposing to effect a transaction in a penny stock to deliver the customer a risk disclosure document that provides certain information prescribed by the Commission, including, but not limited to, the nature and level of risks in the penny stock market. The broker or dealer must also disclose the aggregate amount of any compensation received or receivable by him in connection with such transaction prior to consummating the transaction. In addition, the Commission’s rules also require a broker or dealer to make a special written determination that the penny stock is a suitable investment for the purchaser and receive the purchaser’s written agreement to the transaction before completion of the transaction. The existence of the Commission’s rules may result in a lower trading volume of our common stock and lower trading prices.

We do not anticipate declaring any cash dividends on our common stock.

We have never declared or paid cash dividends on our common stock and do not plan to pay any cash dividends in the near future. Our current policy is to retain all funds and any earnings for use in the operation and expansion of our business. If we do not pay dividends, our stock may be less valuable to you because a return on your investment will only occur if our stock price appreciates.

The Securities issued in our recent private placements may dilute your percentage ownership interest and may also result in downward pressure on the price of our common stock.

In connection with our private placements in September 2012 and January 2013, we issued convertible debentures and warrants which are convertible into or exercisable for an aggregate of 17,650,000 shares of our common stock. If all such shares of common stock were issued, our stockholders would experience a dilution in ownership interest of approximately 8.7%. In addition, as we are required to register these shares for resale by the holders, it is possible that a significant number of shares could be sold at the same time. Because the market for our common stock is thinly traded, the sales and/or the perception that those sales may occur, could adversely affect the market price of our common stock. Furthermore, the mere existence of a significant number of shares of common stock issuable upon conversion of the debentures or the exercise warrants may be perceived by the market as having a potential dilutive effect, which could lead to a decrease in the price of our common stock.

18

Item 1B. Unresolved Staff Comments.

None.

Item 2. Properties.

We lease approximately 12,000 square feet of office and laboratory research facilities at 900 Walt Whitman Road, Melville, New York (our principal offices) from an unrelated party pursuant to a lease that expires November 30, 2014. Our base rent is approximately $312,000 per annum and the lease provides an escalation clause for increases in certain operating costs. See Note 7 to our Consolidated Financial Statements.

We have begun to vacate and return certain portions of our facilities to the landlord for possible re-letting.

Item 3. Legal Proceedings.

On January 28, 2013, we filed a lawsuit in the United States Federal District Court for the Northern District of California against AUO and E Ink in connection with the EPD License Agreement and the Nano Display License Agreement, alleging breach of contract, breach of the implied covenant of good faith and fair dealing, fraudulent inducement, unjust enrichment, unfair business practices, attempted monopolization, and other charges, and we are seeking compensatory, punitive, and treble damages. A copy of the Complaint filed in the AUO/E Ink Lawsuit is available at www.CopyTele.com.

In addition to numerous and continual material breaches by AUO of the EPD License Agreement, and the Nano Display License Agreement, the Complaint alleges that AUO and E Ink conspired to obtain rights to CTI’s ePaper® Electrophoretic Display technology, and CTI’s Nano Field Emission Display technology, through an elaborate scheme whereby AUO obtained certain rights to the technologies under the guise of jointly developing products with CTI, which products would compete with certain products manufactured by AUO and certain products manufactured and sold by E Ink. Instead of jointly developing products with CTI and competing with E Ink, AUO clandestinely agreed to sell its electrophoretic display business to E Ink, and attempted to include a license to CTI’s ePaper® Electrophoretic Display technology as part of the sale, with CTI receiving no consideration. CTI alleges that such activities violated several State and Federal anti-trust and unfair competition statutes for which punitive and/or treble damages are applicable.

On January 28, 2013, we also filed a separate lawsuit against E Ink for patent infringement. See “Item 1. Business – CTI’s Patent Portfolios – Patent Monetization and Patent Assertion Actions”.

Other than the foregoing, we are not a party to any material pending legal proceedings. We are party to claims and complaints that arise in the ordinary course of business. We believe that any liability that may ultimately result from the resolution of these matters will not, individually or in the aggregate, have a material adverse effect on our financial position or results of operations.

19

Larounis, former director of the Company, at a price of $0.1786 per share, or proceeds of $1,250,000. In conjunction with the sale of the common stock, we issued the investors warrants to purchase 7,000,000 unregistered shares of our common stock. Each warrant grants the holder the right to purchase one share of our common stock (or 7,000,000 shares of common stock in the aggregate) at the purchase price of $0.1786 per share on or before February 8, 2016. Certain of the investors are officers and/or directors of the Company and the warrants issued to such persons included a “cashless exercise” provision.

On September 12, 2012, we completed a private placement with 5 accredited investors, including Lewis H. Titterton, the Company’s Chairman and then Chief Executive Officer, and Bruce Johnson, a director of the Company (the “Investors”), pursuant to which we sold $750,000 principal amount of 8% Convertible Debentures due 2016 (the “Debentures”). The Debentures mature on September 12, 2016, bear interest at the rate of 8% payable quarterly and are convertible into shares (the “Conversion Shares”) of our common stock of the Company, and at a price per share of $0.092. The Company may prepay the Debentures at any time without penalty upon 30 days prior notice. The Debentures also provide for events of default which, if any of them occurs, would permit the principal of and accrued interest on the Debentures to become or to be declared due and payable, unless the event of default has been cured or the holder of the Debenture has waived in writing the event of default. The Company granted the holders customary piggy-back registration rights. If all of the Debentures are converted, the Company would issue 10,870 shares of its common stock for each $1,000 principal amount of Debentures or 8,152,174 shares of its common stock in the aggregate.

On September 19, 2012, the Board granted stock options to purchase 41.5 million shares. Of these options, options to acquire 40 million shares were issued to the new management team and have an exercise price of $0.2175. Twenty million of those options will vest only if certain milestones are met. The remaining options to acquire 1.5 million shares were issued to Lewis H. Titterton, the Company’s Chairman, and Kent Williams, a director of the Company and have an exercise price of $0.2225. For additional information with respect to the options, see “Item 12 – Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters – Executive Compensation – Equity Compensation Plan Information” below.

On January 25, 2013 (the “Closing Date”), we completed a private placement with 20 accredited investors, including Robert A. Berman, the Company’s President, Chief Executive Officer and a director, Dr. Amit Kumar, a consultant and director of the Company, and Bruce Johnson, a director of the Company (the “Investors”), pursuant to which we sold $1,765,000 principal amount of 8% Convertible Debentures due 2015 (the “Debentures”) and warrants (the “Warrants”) to purchase 5,882,745 shares of common stock of the Company, par value $0.01 per share (the “Warrant Shares”). The Debentures mature on January 25, 2015, bear interest at the rate of 8% payable quarterly and are convertible into shares (the “Conversion Shares”) of our common stock at a price per share of $0.15. The Company may prepay the Debentures at any time without penalty upon 30 days prior notice, but only if the sales price of the common stock on the principal market on which the common stock is primarily listed and quoted for trading is at least $0.30 for 20 trading days in any 30-day trading period ending no more than 15 days before the Company’s prepayment notice.

21

The Debentures contain full ratchet anti-dilution protection which means, that, subject to certain exceptions, if the Company sells shares of common stock (or securities convertible or exchangeable into common stock) at an effective price of less than $0.15 per share of common stock, the conversion price of the Debentures will be reduce to such lower effective sales price.” The Debentures also provide for events of default which, if any of them occurs, would permit the principal of and accrued interest on the Debentures to become or to be declared due and payable, unless the event of default has been cured or the holder of the Debenture has waived in writing the event of default. If all of the Debentures are converted, the Company would issue 6,667 shares of common stock for each $1,000 principal amount of Debentures or 11,767,255 shares of its common stock in the aggregate. For each $1,000 principal amount of Debentures, the Company issued a Warrant to purchase 3,333 shares of common stock. Each Warrant grants the holder the right to purchase the Warrant Shares at the purchase price per share of $0.30 on or before January 25, 2016. If there is not an effective registration statement covering the Warrant Shares, the Warrants may be exercised on a cashless basis.

Pursuant to the Debentures and Warrants, no Investor may convert or exercise such Investor’s Debenture or Warrant if such conversion or exercise would result in the Investor beneficially owning in excess of 4.99% of our then issued and outstanding common stock. A holder may, however, increase this limitation (but in no event exceed 9.99% of the number of shares of common stock issued and outstanding) by providing the Company with 61 days’ notice that such holder wishes to increase this limitation.

In connection with this offering, the Company granted each Investor registration rights with respect to the Conversion Shares and the Warrant Shares. The Company is obligated to use its reasonable best efforts to cause a registration statement registering for resale the Conversion Shares and the Warrant Shares to be filed no later than 90 days from the Closing Date and must be declared effective no later than 180 days from the Closing Date. The Company is required to use it reasonable best efforts to keep the registration statement effective date until the Conversion Shares and the Warrant Shares can be sold under Rule 144(k) of the Securities Act or such earlier date when all Conversion Shares and the Warrant Shares have been sold publicly; provided, however, the Company shall not be required to keep the Registration Statement effective for a period of more than three years from the Closing Issuance Date. If a registration statement covering the resale of the Conversion Shares is not filed within the 90-day period (the “Filing Default”), then on the date of the Filing Default and on each monthly anniversary (if the Filing Default has not been cured by such date) until the Filing Default is cured, the Company shall pay in cash to each Debenture holder liquidated damages equal to 1.0% of the aggregate purchase price paid by such holder for such Debentures then held by such holder. The liquidated damages will apply on a daily pro-rata basis for any portion of a month prior to curing of the Filing Default. The Company will not be liable for liquidated damages with respect to Warrant Shares.

In connection with this offering we paid The Benchmark Company LLC, as placement agent, a cash placement fee of $41,400 (or 6% of the aggregate purchase price from the investors they introduced to us) and issued to them warrants to purchase 276,000 shares of common stock (or 6% of the aggregate number of shares underlying the Debentures issued to the investors they introduced to us) upon the same terms as the Warrants issued in the offering.

22

The issuances of the securities referred to above (i) were not registered under the Securities Act of 1933, as amended, in reliance on an exemption from registration under Section 3(b) or Section 4(2) of the Act, and Rule 506 promulgated thereunder, based on the fact that all of the investors are “accredited investors,” as such term is defined in Rule 501 of Regulation D and (ii) were not subject to any underwriting discounts or commissions.

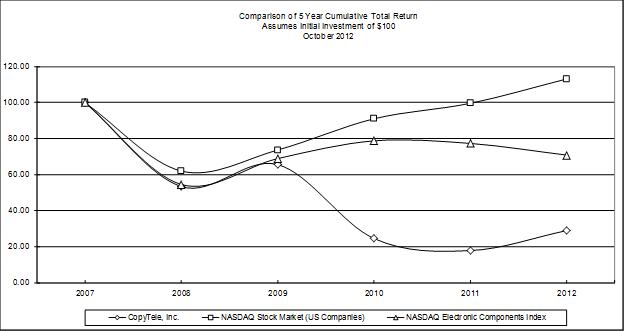

Stockholder Return Performance Graph

Set forth below is a graph showing the five-year cumulative total return for: (i) our common stock; (ii) The Nasdaq Stock Market U.S. Index, a broad market index covering shares of common stock of domestic companies that are listed on The Nasdaq Stock Market (“Nasdaq”); and (iii) The Nasdaq Electronic Components Stock Index, a group of companies that are engaged in the manufacture of electronic components and related accessories with a Standard Industrial Classification Code of 367 and listed on Nasdaq.

|

|

| Fiscal Year Ended October 31 | |||||

|

|

| 2007 | 2008 | 2009 | 2010 | 2011 | 2012 |

|

|

|

|

|

|

|

|

|

| COPYTELE INC | Cum $ | 100.00 | 53.33 | 65.54 | 24.44 | 17.77 | 28.88 |

|

|

|

|

|

|

|

|

|

| NASDAQ Stock Market (US Companies) | Cum $ | 100.00 | 61.93 | 73.63 | 90.96 | 99.54 | 113.10 |

|

|

|

|

|

|

|

|

|

| NASDAQ Electronic Components Index | Cum $ | 100.00 | 54.48 | 68.82 | 78.69 | 77.26 | 70.76 |

23

The comparison of total return on investment for each fiscal year ended October 31 assumes that $100 was invested on November 1, 2007 in each of CopyTele, The Nasdaq Stock Market U.S. Index and The Nasdaq Electronic Components Index with investment weighted on the basis of market capitalization and all dividends reinvested.

Issuer Purchases of Equity Securities

None.

Item 6. Selected Financial Data.

The following selected financial data has been derived from our audited Consolidated Financial Statements and should be read in conjunction with those statements, and the notes related thereto, which are included in this Annual Report on Form 10-K.

|

| As of and for the fiscal years ended October 31, | ||||

|

| 2012 | 2011 | 2010 | 2009 | 2008 |

| Net revenue | $947,085 | $1,003,193 | $ 730,675 | $1,055,797 | $ 2,063,123 |

| Cost of encryption products sold | 3,873 | 34,081 | 38,441 | 27,861 | 95,594 |

| Provision for excess inventory | - | - | 43,866 | 19,627 | - |

| Cost of display engineering services | - | - | - | 18,200 | - |

| Research and development expenses | 2,211,506 | 3,124,773 | 3,007,459 | 4,116,200 | 4,127,393 |

| Selling, general and administrative expenses | 2,866,262 | 2,872,605 | 2,889,129 | 4,194,227 | 3,829,654 |

| Impairment in value of available for sale securities | - | 1,785,793 | - | 9,218,972 | - |

| Interest expense | 7,664 | - | - | - | - |

| Dividend income | 13463 | 33,507 | 68,211 | 29,468 | 130,886 |

| Interest income | 3,458 | 2,516 | 4,878 | 20,807 | 37,028 |

| Provision for income taxes | - | 600,000 | - | - | - |

| Net loss | (4,252,799) | (7,378,036) | ( 5,175,131) | (16,489,015) | (5,821,604) |

| Net loss per share of common stock – basic and diluted | ($.02) | ($.04) | ($.03) | ($.12) | ($.05) |